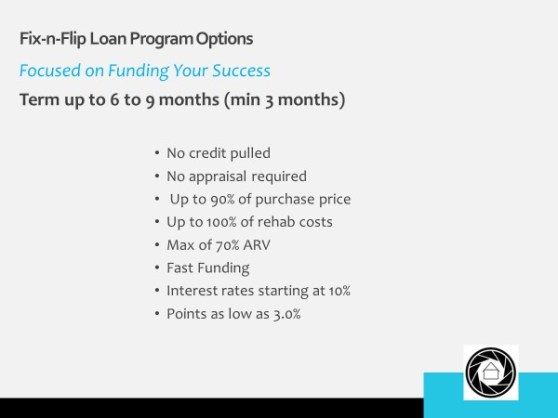

Attention. Today, it is hard to focus the laser beam of our mind onto what is pivotal. Our mind certainly can be a laser beam, but too often it flickers, back and forth from one thing to another like a match in a wind storm. If time is money, attention is gold, and a sense of urgency can be your friend when you are interested in borrowing money to start your rental or vacation rental business.

My goal here is to help you sort out what Visio needs to know, what is pivotal in the process of financing an investment property, one that you want to buy and hold onto as an investment. By focusing on these critical areas, you can speed up and simplify the process of getting your loan Visio loan closed.

Pivot 1. Property Value beyond the Appraisal

Talk to your local realtor and do your own research to determine the comparable value of your property. Appraisals provide us with helpful indications of value, but we also rely heavily on our own research and analysis. Please let us know if you’ve made improvements to the home, detailing what has been done and the amounts invested.

Please let us know if you’ve made improvements to the home.

Pivot 2. Property Condition

Appraisers rate property condition using a scale of C1 (New) to C6 (Complete Redevelopment). We only lend on rent-ready properties (C1–C4). ALL repairs and rehab should be completed PRIOR to starting a loan with Visio. While we sometimes finance properties requiring some minor redevelopment, we make these decisions on a case-by-case basis. If you are concerned that your property may need too much work to qualify, send us some current pictures before ordering the appraisal.

We only lend on rent-ready properties (C1–C4).

Pivot 3. Recent Transactions

If the home has changed hands in rapid succession with significant increases in value, we need to know ahead of time. We need to understand the reasons behind the increase in value before making the loan. Finding out late in the transaction almost always causes problems.

We need to understand the reasons behind the increase in value before making the loan.

Pivot 4. Non-Arm-Length Transactions

A non-arms-length transaction involves a buyer and seller that have a pre-existing business, personal, or familial relationship. We will make these loans, but we want to know up front. Visio is not a consumer mortgage lender, and therefore cannot allow family of the borrower to remain in the property.

Visio is not a consumer mortgage lender, and therefore cannot allow family of the borrower to remain in the property.

Pivot 5. Fees

Our Account Executives will provide you with a detailed fee worksheet showing all our fees well in advance of closing. Please read the fee worksheet. It is not in anyone’s interests to have a deal fall apart at the closing table over fees.

Please read the fee worksheet.

Pivot 6. Title

If you are refinancing with Visio please give careful thought to any liens, judgments, or delinquent property taxes on the property. These will come up during the title phase, and they not only take time to clean-up but could also result in disqualification. If you’re buying a property, we require a clean title to close. Items such as releases of old mortgages or the existence of ground rents/land leases, which are common in some areas (MD), can take substantial time and effort to address.

We require a clean title to close.

Pivot 7. Borrower Name(s)

If you are refinancing with Visio, please consider whether there is anyone else on the title with you. That person will need to be available to sign documents. In addition, we will title the property the way it comes to us. If you are attempting to remove anyone from or add anyone to title, please resolve this prior to starting a loan with Visio (see “Borrowing in an Entity” below for exceptions). For purchases, if you are buying from a government agency, such as HUD, execute the purchase contract in the exact name in which you intend to hold the title. They are not very flexible about changing names mid-transaction.

Execute the purchase contract in the exact name in which you intend to hold the title.

Pivot 8. Investor Insurance

Research and choose your insurance product EARLY. It likely will take longer than you think. Consider the cost as well. If your premium is proven to be more expensive than you are estimating, it could potentially change your loan parameters, up to, and including disqualification. Accurate escrow estimation is paramount to an accurate quote from Visio. Please note, we require hazard insurance to have 100% replacement cost. We do not allow actual cash value policies.

We require hazard insurance to have 100% replacement cost.

Pivot 9. Borrowing in an Entity

We lend to entities, such as corporations, LLCs, and partnerships. Please make sure your entity is fully established and is in good standing. We’ll need all the documents to complete your loan. If you are attempting to change the titled entity, we can accommodate if the ownership interest is identical between both entities. (See “Borrower Name” above.) We do NOT lend to trusts nor non-profit corporations.

We do NOT lend to trusts nor non-profit corporations.

Pivot 10. Sense of Urgency

Time and attention is always of the essence. Thoroughly read emails and respond to communication from your account executive and processor. We are always available to help and provide clarification to ensure a smooth transaction.

Thoroughly read emails and respond.

Give me a call or send an e-mail and I will help you to move quickly, get the best deal, and start making money sooner.

Patrick@InvestorsLendingSource.com

512-213-2271

Austin, Texas

Photo reference: Lmatt123 [CC BY 3.0 (https://creativecommons.org/licenses/by/3.0)%5D

Next, get a remodeling contractor to give you a bid on the repairs and a plan or time frame the repairs will take. You might want to get several bids and choose the one that looks best to you.

Next, get a remodeling contractor to give you a bid on the repairs and a plan or time frame the repairs will take. You might want to get several bids and choose the one that looks best to you.